Vs Financing Vs Leasing a Vehicle: Cars are an indispensable part of modern life. We use cars for various driving purposes, be it taking kids to and from school, transporting goods to various places, or traveling to different destinations.

There comes a time when you might consider replacing your car and be thinking about the best way to go about it. You have three choices: buying, financing, or leasing. It is often tough to determine the best option to choose.

This article will discuss the different options and clarify what they mean to you, including their advantages and disadvantages. Buying means you pay the vehicle’s price entirely before owning it. Financing involves making monthly payments for a set period of time after which the car is yours. Finally, leasing involves making monthly payments meant to secure the rights to use and enjoy the car for the period, at the end of which you return it and walk away.

Leasing

Leases have simple contracts where you pay the car for a certain period and range unless you go over the limits or cause any damages. Leasing is similar to rent but usually involves more extended periods of time. The car is pretty much yours for the lease period, but you have to return it when the term expires, after which you can either enter a new agreement, buy or finance it.

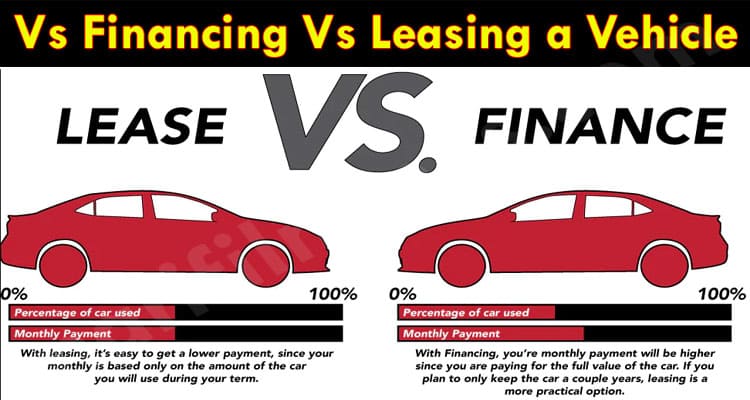

This option’s main benefit is that it has few upfront costs. Most of the time, you are only asked to post a refundable security deposit, the first month’s payment, and other fees. In addition, lease payments are always lower than those that come with financing.

The main reason is that you are only paying for depreciation when you lease a vehicle. Leasing allows you to drive cars during a period when they give the least trouble. Leases are usually for new vehicles, meaning you get to drive an automobile that will require minimum maintenance and cause minimum inconveniences.

Given cars for lease are almost always new, so you get to drive them at a time when manufacturer warranties cover them. This means you will pay less no matter what happens to the vehicle. Leases give you the means to drive better automobiles than you can afford. This also means that the cars will have the latest features, meaning you will be driving a safer, more-capable automobile.

Finally, you are also free to switch cars frequently and are not stuck with a model you cannot sell. However, there is a number of significant downsides. A strict limit usually accompanies a lease agreement where there is a maximum range you can cover, and any violation, no matter how slight, can be accompanied by significant penalties. Besides, if you maintain the car poorly and it has significant wear and tear, you will have to make additional payments. In addition, sometimes, you may want to terminate the lease early because of unforeseen circumstances, but that often means still paying the full amount or paying a termination fee.

You are not allowed to customize the car according to your tastes and preferences and are required to return it in a condition similar to the one in which it left the lot. Leases end up costing a lot because you pay for a car at a time when it depreciates the most.

Financing

This option is pretty much the same as a mortgage; you have a contractual agreement with a creditor and make payments to settle the principal and interest. This arrangement means monthly payments over a given period of time. The entire cost of the car, fees and taxes are included in the payment. There are a number of upsides and downsides to financing.

The most significant advantage is that the car is yours after clearing your loan. If you desire, you can sell the vehicle and use the funds to make a down payment for a new loan, pay down other debts, or make other purchases. Other advantages include:

- You are not limited on the distance you can cover while making payments like with a lease. This means you can drive any number of miles, but you should keep in mind that a car’s resale value is directly related to the number on its odometer.

- You can trade-in your car or sell it whenever you don’t want it anymore without extra charges like in a lease.

- Financing is one of the best ways to build your credit score. The monthly payments are a good indicator of your credibility, so you can use them to secure other bigger loans for investment or other purposes.

The main con of this option is that the associated monthly payments are usually much higher than those associated with leases because they take into account the car’s purchase price, interest, and other miscellaneous charges. Also, when you finance a vehicle, it is used as collateral for the owed amount.

Therefore, any later payments could result in a repossession, increased interest rates, hefty fees, and serious damage to your credit score. There are also instances where you could be stuck in a lengthy contract, and you end up paying more for the car than it is worth.

Buying

This option is for those people with funds to cover the entire price of the desired model. The appeal of this choice lies in the fact that you don’t have to pay extra money in the form of interest like with leasing or financing. Paying fully for a car gives you the right to modify and customize it according to your tastes and preferences.

You have the last word on what you want to happen to the car. New cars come with a warranty that you can take full advantage of and keep your vehicle in crisp condition while it lasts. You also do not need to worry about your credit score or history as you have all the funds.

While this may sound like the best way to go if you have the resources, many loans and leases today are low-interest, meaning you won’t incur many expenses if you go with either. With that, car dealerships and showrooms offer a number of cash incentives that increase this option’s allure.

Besides, you could put the money you would have used to make an upright payment towards other investments and projects that would give you a higher return than the interest you would have paid for the vehicle’s financing or lease. You will need to take a close look at this option if you believe your investments will generate enough money to cover the costs of a loan or lease. If this is the case, leasing or financing may be the best way to go.

The main downside of buying a car is that it depreciates over time. A car can lose up to 40% of its purchase value within five years.

Conclusion

There comes a time when your car does not meet your requirements or preferences, and you are looking for a replacement. Today’s car market is a very expensive market replacing a car is a hefty situation to find yourself in. You can buy, lease, or finance your next vehicle, and any choice depends on what you are looking for in an automobile that best fits your needs and preferences.